If you’re comparing a Roth IRA to a 529 Plan, you’re in good company. While 529 Plans are often the first consideration for education savings, Roth IRAs can also offer valuable tax benefits. Understanding the differences between the two strategies can help you feel confident making a choice that supports your child’s future and fits your broader financial goals.

The Importance of Early Planning

College costs can feel overwhelming. For the 2024–2025 academic year, theCollege Boardreports that the average total cost (tuition, fees, room, and board) for an in-state public university is about $24,030 per year, while for a private nonprofit four-year college it’s about $56,190 per year.1

Tuition and fees alone average around $11,260 for in-state public students and $42,100 for private nonprofit students.1That represents a roughly 2.2% increase from the prior year, in line with U.S. Bureau of Labor Statistics data showing college tuition and fees rising 2.2% year-over-year through August 2025.2And that’s just for undergrad — graduate school or other advanced programs could push that total even higher.

It’s a lot to think about, especially when you're trying to balance other financial priorities. But here’s the good news: starting early gives you options. The sooner you begin saving — especially in a tax-advantaged account — the more time your money has to grow and work for you. Even small, consistent contributions can add up over time and help ease the burden when tuition bills arrive.

Option 1: 529 College Savings Plan

Think of a 529 Plan as a dedicated education savings account. It’s built specifically for school-related expenses and comes with some powerful perks:

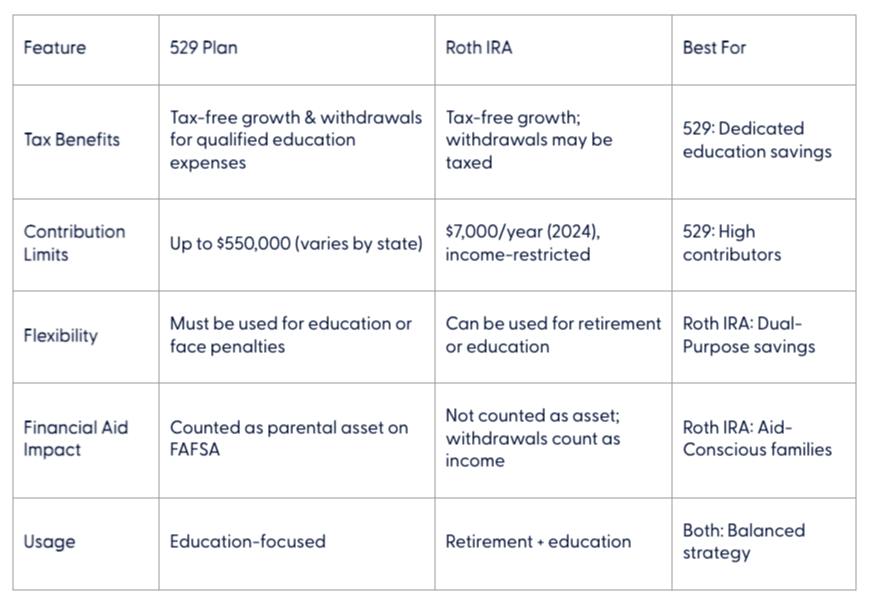

- Tax-free growth and withdrawals for qualified education expenses

- High contribution limits (up to $550,000 depending on your state)

- Can be used for college, K–12 tuition, and even student loan repayment

- Some states offer tax deductions or credits for contributions

If your goal is to save specifically for education and you want to maximize tax benefits, a 529 Plan is a strong contender.

Option 2: Using a Roth IRA for College

Roth IRAs are traditionally used for retirement, but they can also play a role in education savings. Here’s how:

- You can withdraw contributions anytime, tax-free

- Earnings can be used for qualified education expenses without the 10% early withdrawal penalty (though income tax may apply)

- Roth IRAs don’t count as assets on the Free Application for Federal Student Aid (FAFSA), which may help with financial aid

- However, withdrawals do count as income two years later, which could affect aid eligibility

If you’re already on track with retirement savings and want flexibility, a Roth IRA can be a smart dual-purpose tool.

Side-by-Side Comparison: Roth IRA vs. 529 Plan

When to Use One — or Both

There’s no one-size-fits-all answer when it comes to using a 529 plan or Roth IRA to fund educational expenses. Your choice depends on your goals, timeline, and how much flexibility you want.

- Use a 529 Planif you’re confident the funds will go toward education and want to maximize tax benefits.

- Use a Roth IRAif you want flexibility and are already saving for retirement.

- Use bothto hedge your bets — especially if your child’s education path isn’t set in stone.

Next Steps: Build Your College Savings Strategy

Here’s how to get started:

- Estimate future education costsbased on your child’s age and school plans.

- Explore your state’s 529 Planoptions and tax benefits.

- Review your retirement savingsbefore using a Roth IRA for college.

- Talk to a financial advisorto coordinate your savings strategy.

Consider using both accountsto balance flexibility and tax efficiency.

----------------------------------------------------------------------------------------------------------------------------------------------------------------------

1. “Trends in College Pricing and Student Aid 2024”, College Board, 2024.

2. “Consumer Price Index”, U.S. Bureau of Labor Statistics, August 2025.

Disclosures

Prior to investing in a 529 Plan investors should consider whether the investor's or designated beneficiary's home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state's qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

A Roth IRA offers tax deferral on any earnings in the account. Qualified withdrawals of earnings from the account are tax-free. Withdrawals of earnings prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Limitations and restrictions may apply.

Tracking #820976