A key part of financial wellness is the ability to manage competing financial goals while optimizing your saving and investment opportunities. While the order may be different based on your own personal situation, the following foundational tips can help you prioritize to get the most bang for your saving bucks.

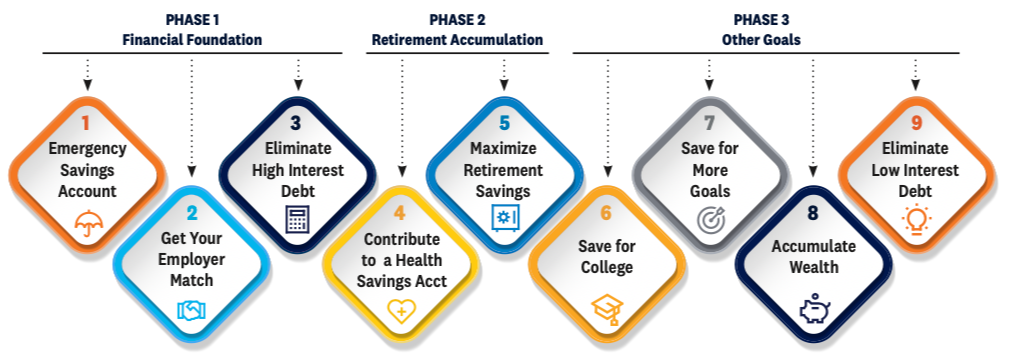

PHASE 1: FINANCIAL FOUNDATION

1. Fund an Emergency Savings Account. Unplanned expenses make it hard to sustain a consistent saving strategy (and

possibly lead to high interest credit card debt). Think: car repair, dishwasher replacement, leaky roof, or worse — an unexpected gap in employment. Build up a fund in a liquid, accessible savings account until it holds at least three to six months of living expenses (preferably closer to six).

2. Get Your Employer Match. Make sure you are contributing enough to your workplace retirement plan to receive the full employer match. This is free money. For example, a common employer matching formula is to contribute $0.50 for each dollar you contribute, up to 6% of your pay. That’s a 50% return on your investment. A dollar for dollar employer match up to a certain percentage of your pay is even better — a 100% return on your investment!

3. Eliminate High Interest Debt. Credit cards are often your most expensive debt. And if you use credit cards too much, they can become the biggest obstacle to reaching your financial goals. If you have more than one card with a balance, focus on paying down the one with the highest interest rate first. Or start with lowest balance card, if that’s easier. You can apply this strategy to other debts as well, such as student loans, car loans or home equity loans.

PHASE 2: RETIREMENT ACCUMULATION

4. Contribute to a Health Savings Account (HSA). If offered by your employer, contributions to an HSA are triple tax-free: your contributions are pre-tax, your savings grow on a tax-deferred basis, and withdrawals for qualified medical expenses are tax-free. These unique tax advantages make HSAs an excellent way to save for healthcare expenses you may incur now and in the future, even during retirement. And as a bonus, many HSAs include an employer match (free money again). Flexible Spending Accounts (FSAs) are another place to consider putting your money, as their tax advantages are basically the same as HSAs. One caveat: some FSAs require you to spend the money by year-end.

5. Maximize Your Retirement Savings. Do you still have discretionary saving dollars after taking care of your personal priorities, such as setting up an emergency fund, paying off high interest credit card debt and funding other financial goals? Then it’s time to focus on trying to max out your 401(k), 403(b), IRA

or other type of retirement plan, like a Roth account. While Roth contributions don’t give you a tax deduction now, the withdrawals in retirement are tax-free. In 2024, you can contribute up to $23,000 to a workplace retirement plan, plus an additional catch- up contribution of $7,500 if age 50 or older. For IRAs, the amount is $7,000 plus an additional catch-up contribution of $1,000.

PHASE 3: MORE GOALS

6. Fund College Savings. For most families, a 529 plan is an excellent use of your college savings dollars. While you don’t receive a federal tax deduction, the money grows tax-deferred for the benefit of the student and is not subject to federal taxes when withdrawn for qualified education expenses.

7. Save for More Goals. Maybe you want to take a vacation next year, or you know you will need a new car or want to buy a second home. If so, consider a high interest savings account. Or, if the goal is further out, you may opt for a regular taxable investment account. There are no maximum contribution limits with these types of accounts.

8. Accumulate Wealth. To build up your net worth, you can invest or save money in things like taxable accounts, annuities and cash value life insurance. By diversifying your savings, you have the opportunity for both lower tax bills in retirement and potentially higher returns on your investments.

9. Pay Off Low Interest Debt. Even low interest debt like a low cost mortage or home equity loan can be a burden when you are older and not working. By periodically making extra payments, you could pay off those loans much faster than you thought.

You might be surprised at how satisfying it is to work on becoming debt-free. Gaining control of your finances gives you and your family the opportunity to realize many more of your dreams for the future.

Don’t hesitate to contact us to talk things through. We will help you prioritize your current financial goals, offer guidance on how much to save and how to invest your savings, and follow up with you periodically to discuss your progress.

Important Disclosures:

This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal or investment advice. If you are seeking investment advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

The Roth IRA offers tax deferral on any earnings in the account. Withdrawals from the account may be tax free, as long as they are considered qualified. Limitations and restrictions may apply. Withdrawals prior to age 59 1⁄2 or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Future tax laws can change at any time and may impact the benefits of Roth IRAs. Their tax treatment may change.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 591⁄2 may result in a 10% IRS penalty tax in addition to current income tax.

Prior to investing in a 529 Plan investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

This material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and GENESIS Wealth Management are separate entities.

Tracking #514679 (Exp.11/25)